Should netflix be ‘bingeing’ on brand building?

With inflation rampant across the world, consumers have been trimming their expenses and Australians are no exception. Many have cut back on luxury goods, holidays, eating out, and even subscription services like pay TV. With the average Australian household having 3.5 subscription video on demand (SVoD) services, these brands are now seeing how Australians will treat them during a cost-of-living crisis.

Kantar’s Global Issues Barometer has found 59% of Australians say they are more likely than not to cut back on SVoD, and the percentage of Australian households accessing these services has declined during 2022.

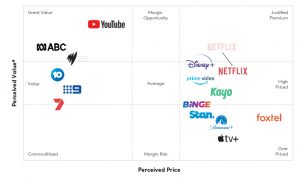

But how has the most iconic brand in the category been faring? Netflix remains the clear market leader, with 4.8 million Australian households subscribing. However, market share is declining, and most new subscriptions are being allotted to competitors such as Amazon Prime Video, Disney+, and Stan. To date, Netflix has implemented consistent price increases and recently announced its intention to upend password sharing, aiming to maintain margin in this increasingly competitive category. However, Kantar BrandZ data shows perceptions of Netflix charging ‘fair prices’ have fallen from 44% of Australians in 2020 to 34% in 2022, with competing brands such as Amazon Prime Video building out a strength in value for money at a consistent price point of A$6.99 per month.

That fee also happens to be the launch price for Netflix’s ‘Basic with Ads’ offering – its response to the inflationary environment with a cost-effective option that takes advantage of a lucrative profit driver: advertising revenue. Our Worldpanel research shows 36% of SVoD households in Australia agree that they wouldn’t mind seeing ads if it made the service cheaper; that’s a smaller proportion than in the US (52%), but still an addressable market.

But is this the optimal route to grow Netflix’s profitability in the long run? Or does Netflix run the risk of reduced revenue from users downgrading their subscription?

So far, Netflix has explored two options to grow profitability: increasing prices and providing a new, lower-price tier. But price is just one side of the two-sided coin of price and value. As Netflix’s price has increased, perceptions of value have remained stable – pushing the brand from having a justified premium to being seen as a high-priced brand, Kantar BrandZ data shows. If a brand wants to retain customers, it’s difficult to increase relative price without having increased perceptions of value. In fact, Netflix’s intentions in ending password sharing could work to reduce perceptions of value.

Prime-time value – how providers compare

* Perceived Value refers to the difference from a brand’s expected Pricing Power. That is, the value that brand is perceived to generate at their given price point.

So how can marketers faced with a similar dilemma maintain their value while shifting their price? The real answer is something Netflix seems to have all but ignored over the years: building a distinctive and differentiated brand.

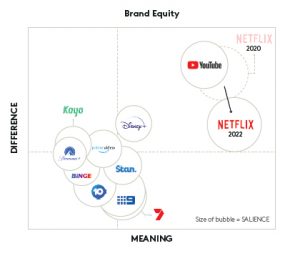

The dimension of Difference

Through Kantar’s work with the Oxford Saïd Business School, we know that a brand’s Difference (that is, whether it is perceived as being unique and/or setting trends) is the strongest factor in determining whether that brand outperforms expectations on the share market. We also know that this relationship is particularly powerful within the SVoD category, where Difference plays even more of a leading role in driving profitability.

As the SVoD category has become more saturated, Netflix’s Difference index has decreased from 162 in 2020 to 122 in 2022. While the brand retains the strongest consumer predisposition in the category, its brand equity profile has shifted away from YouTube. Disney+, on the other hand, is poised to grow, standing out from competing services in terms of Difference.

Time for something different?

As Difference is the core driver of Netflix’s ability to charge a higher price, increased prices without added Difference have led to users increasingly jumping ship. To combat this decline, Netflix needs to look beyond content and reinvest in order to position the brand as unique or setting trends relative to the competition. One area that is ripe for this investment is Netflix’s distinctiveness.

A point of distinction

We know that the most successful brands create a recognisable set of memory structures within consumers’ minds, consistently repeated over time. Netflix is increasingly not one of these brands, having moved from being perceived as a distinctively fun and playful brand to one with no clear brand identity, Kantar BrandZ data shows. This is particularly pertinent when viewed next to competitors such as YouTube and Disney+, which communicate with a consistent and distinctive tone of voice. In a fragmented market, where functional difference is hard to come by, brand becomes ever more important in reducing churn and attracting new users. Netflix’s identity is currently defined more by the tonality of the brand’s content as opposed to the brand’s own distinctive assets. As YouTube and Disney+ more successfully compete for Australians’ eyeballs, Netflix should consider not just bingeing on content, but building a clearer brand identity.

Cameron Dove

Associate Director

Australia, Kantar

This was first published in the Kantar BrandZ 2023 Most Valuable Brands Report – download it here